HLS.ASX

Pathology provider trading <0.4x EV/Revenue albeit loss making – turnaround opportunity with likely imminent special dividend of >40% of todays market cap including franking

This is 100% my personal view and NOT advice - see disclaimer.

HLS.ASX - $1.27

Healius is Australia’s second largest pathology provider with circa 30% market share in what is supposed to be an industry where only those with scale can be profitable – yet today HLS pathology segment pre corporate overheads is making an embarrassingly low EBIT margin of 0.6% for the most recent half and is loss making at the group level. Their smaller listed competitor ACL made 9% in FY24 at a group level - and Sonic the largest player (45% market share) is believed to make >10% but this isn’t disclosed at a segment level.

The simplistic bet today is that HLS can turn this around as prior to FY19 HLS consistently earned 9-10% EBIT margins at the segment level. If they can achieve a group EBIT margin of 6% - that would result in HLS trading on circa 6x EBIT which I believe is too low for an essential services provider. ACL currently trades on 12x and SHL 17x. Below highlights the historical margins of HLS from an outdated broker note (forecasts were clearly missed).

IMMINENT CAPITAL RETURN

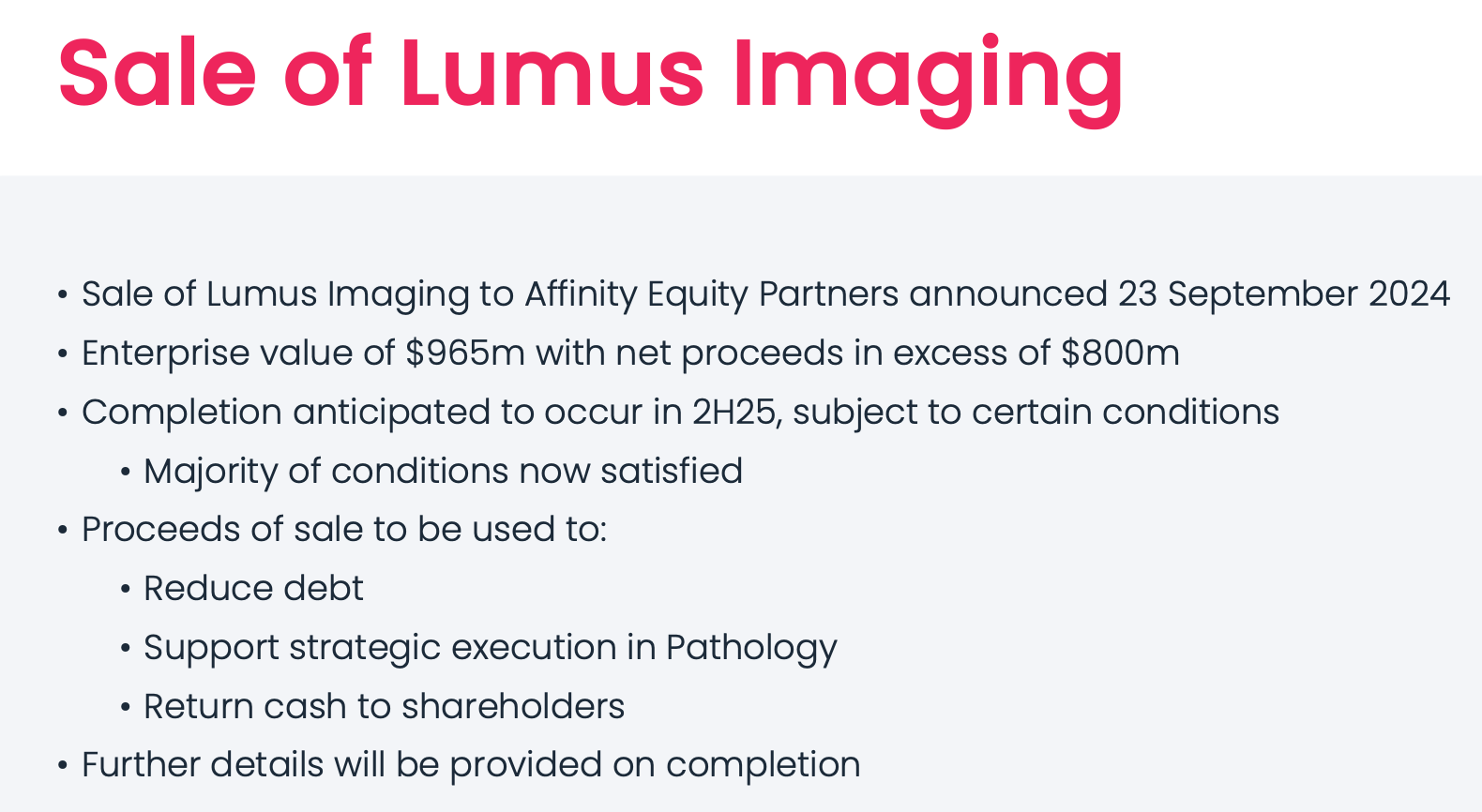

HLS will soon have significant net cash of >400m post selling their profitable imaging division Lumus for 25.4x FY24 EBIT – and I assume will return >300m cash as a fully franked special dividend in the next 3-4 months once the deal settles (a few minor approvals remain which it seems are of minimal risk to the deal completing).

Inclusive of franking credits - this amounts to around 430m value or >45% of the current 920m HLS market cap.

Short term the key risk is the uncertainty around how much HLS will return.

At the November 2024 AGM HLS stated “Healius has $161 million of franking credits. So within the context of maintaining minimal levels of debt in the near term, on the completion of the Lumus Imaging sale, it is our intention to return the majority of proceeds following the repayment of debt to shareholders via a special dividend”.

They also stated in the recent 1H25 results that proceeds will be used to “support strategic execution in pathology” – this amount remains unclear but given in 2018 they first announced a $100m investment into their “laboratory Information System / LIS” and then two “sustainable improvement programs / SIP” – hopefully the remaining investment required to deliver profitability is minor but certainly a risk.

EBIT margins today are 0.6% which is actually much worse if you adjust for the circa 2% points of revenue as “lease interest” below this reported line - so it’s more like negative -1.4% on that basis before adjusting for corporate / overhead costs of another circa 1%? So the capex has clearly failed to date and HLS is burning FCF on a continuing business basis. Below is from the ACL merger presentation in 2023 highlighting these issues:

HLS net debt at 1H25 was 345m – so if we assume that is repaid in full – the Lumus proceeds net of all cash costs >800m – there should be circa 450m net cash once the deal completes absent any further capex and losses. Hence broker forecasts range from 300m-400m from what I’ve seen re the dividend.

Given the shocking capital allocation history of HLS – I suspect the register will be pushing for as much capital including the 161m of franking credits to be released. Tanarra who has been vocal on HLS underperformance (see Appendix) has a board seat and owns 12% - along with Perpetual at 11% - plus two industry super funds who I assume would appreciate the franking credits returned.

VALUATION

Above shows the theoretical valuation of HLS using a 6% EBIT margin and ACL figures are my estimate of their FY25 results - they are soon to report 1H25 results.

Looking at HLS pre dividend and thus before the benefits of any franking – the market cap is 920m at $1.27 and an EV of circa 470m - once Lumus has settled - and an EV/Revenue of <0.4x.

This compares to ACL the number three player at circa 770m EV and EV/Rev of around 1x. ACL is currently generating solid margins despite its smaller scale – however in 2019 just prior to Crescent the Private Equity owners floating the company – ACL was loss making per below from their prospectus. At risk of being grossly simplistic on that basis alone I believe over the next 3 years HLS will be able to turn around their business if management can execute.

There are mix differences suggesting lower structural margins for HLS who is more exposed to GP’s and less specialists / hospitals – however even if we return to 6% margins well below that of ACL – HLS will trade around 6x EBIT.

The key difference between ACL/HLS is labour expenses of circa 49-50% at HLS and ACL at 43% - rent and consumables the other two major expenses are roughly in line.

Paul Anderson the current HLS CEO was appointed March 2024. He was previously CFO and appointed in March 2023 when the previous CFO Maxine Jaquet became CEO (also previous CFO) – however she didn’t last long given the events I’ll come to. Paul today is unproven in Pathology - he was previously CEO of the media company Network Ten albeit is not to blame for HLS shocking capital allocation decisions of the recent past.

M/A + Corporate appeal

ACL bid for HLS in in March 2023 - citing 95m of synergies available on combination. It was all scrip and a 0.74x ratio for every 1 ACL share – implying a price today for HLS over $2.70 and double today’s price. The ACCC flagged issues with this merger so I am not optimistic they will return despite recent press suggesting it was live again. Paul Anderson on the recent earnings call said “that was complete news to us… there is nothing that we're aware of that is happening” which is disappointing – if those synergies are even half achievable HLS should be pursuing such a value enhancing merger.

Furthermore HLS in 2019 was bid for by Jangho at $3.25 which they rejected – good call team! But then also rejected a bid from Partners group in early 2020 at $3.40 – an even worse call given the stock trades at $1.25 today.

HLS subsequently in June 2020 sold their GP business for circa 500m or 10x earnings – then bought Agilex for 300m - a clinical testing business for 10x revenue! and subsequently impaired near half of that purchase as it just delivered 1.1m EBIT for the 1H25 – miles below their initial targets for the business.

HLS made a windfall profit from COVID testing – pathology alone made over 750m EBIT in the two years of 2022/2023 – so HLS decided to buy back stock well over $4 (top price paid was $4.57). But then the COVID boom ended – HLS was over-levered and had to ask for the money back in an emergency rights issue at $1.20 less than a year later – over 70% below the price they were buying back stock for.

Hence my belief the register will push hard for the maximum return possible given that history of capital misallocation.

Lastly If HLS continues to languish at such a poor EV/Revenue multiple of <0.4x – it wouldn’t surprise to see renewed M/A interest – especially as despite the capital return HLS will have little to no gross debt and will likely be net cash – perfect for a private buyer who can lever up the business and could take a longer term view of the potential turnaround and upside.

RISKS

My interest is firstly around the upcoming dividend so this could underwhelm – details should be released at the upcoming investor day March 27, 2025. HLS could retain more for further capex to restore profitability which would disappoint. If they return 300m which is my base case - that still leaves circa 150m net cash which seems excessive.

As always, the turnaround could take longer than expected – HLS is a high fixed cost business - wages and rent will continue to rise – and the business has effectively no net tangible assets despite a significant collection clinic and laboratory footprint which is hard to replicate. These I believe are all leased hence the >900m of lease liabilities on the balance sheet that I exclude from net debt.

I am no expert in pathology and some believe HLS still has too many IT systems – and is less profitable than peers due to the mix issues I mentioned. Lost collection centres / volumes have temporarily impaired the business which I believe can be recovered. 4Cyte - another smaller competitor backed by the Bateman family who ironically started Primary Healthcare that was later renamed HLS - has been taking share. It seems despite an enormous COVID windfall profit their business is now roughly breaking even so maybe HLS isn’t the only one struggling?

The government also recently reduced funding to certain pathology tests and wants to reduce unnecessary testing - so despite the industry crying poor that indexation for pathology testing hasn’t changed in over two decades – HLS will always be subject to changes in government policy and funding. This could however become a tailwind if they do introduce indexation on what HLS is paid per test which is probably fair given the increase in costs.

Ultimately the bet today is that HLS can achieve a fair margin on providing an essential service – either under the current management / ownership or this may need to change to deliver such an outcome.

Below shows the volume growth of the industry from a recent ACL presentation and we will always need blood tests despite the Theranos home testing risk and most know how that ended. HLS just delivered 7% increased revenue for 1H25 – so given they have the balance sheet to deliver a turnaround - no risk of dilution again plus a cheap starting point and imminent capital return – in my opinion HLS today is a mis-priced turnaround bet.

Charlie Kingston

Director

CSK Capital Pty Ltd

Disclaimer

Do not interpret anything above as financial advice. This article has been prepared by the author, CSK Capital Pty Ltd for informational & educational purposes only. The writing contains certain forward-looking statements and opinions which are based on the Author’s analysis of publicly available information believed to be accurate and reliable. While the Author believes that such forward-looking statements and opinions are reasonable, they are subject to unknown risks, uncertainties and other factors that could cause actual results to differ materially from those projected. As of the date the Report is published, the Author may or may not hold a position in the security mentioned and may trade the security in future. Nothing in this Report constitutes investment advice. Readers should conduct their own due diligence and research and make their own investment decisions.

APPENDIX / LINKS

Tannara presentation and recent letters to HLS:

ACL / HLS 2023 merger presentation: